Weekly highlights

Ocean rates out of Asia were stable again this week – though Asia to US West Coast prices did increase and are now level with prices in early October. This suggests that the sharp drop off that began this summer may be leveling out as capacity is removed to meet falling demand.

The latest National Retail Federation data on US container imports estimate that October volumes were about even with September and 9% lower than last October. November and December volumes are projected to dip 5% to the lowest level since February of 2021, but would still represent double digit increases compared to those same months in 2019.

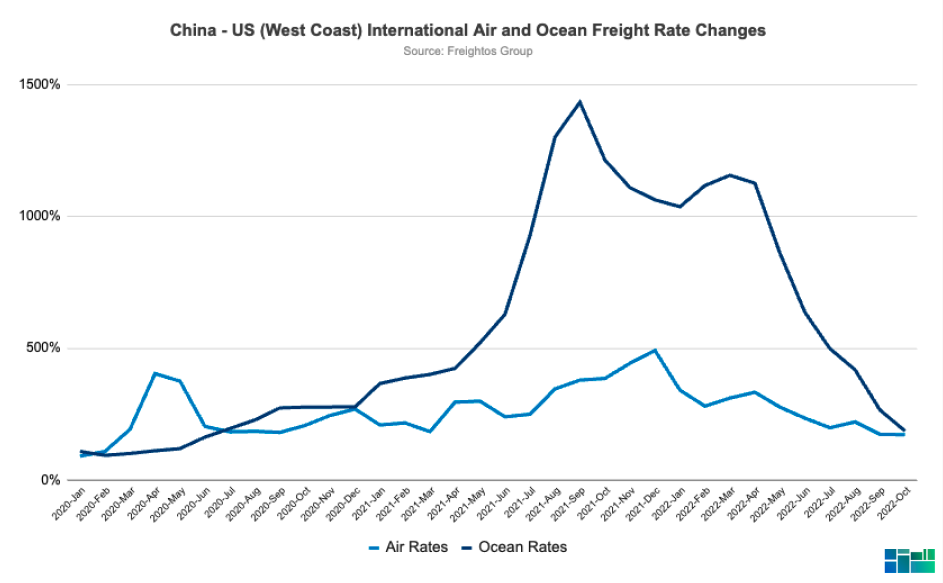

Strong volumes – together with congestion and reductions in capacity – are keeping ocean rates elevated, with ex-Asia rates to the West Coast 81% higher than in November 2019, East Coast rates more than double, and prices to Europe more than triple compared to 2019 levels.

Labor disputes continue to loom in several areas across the globe. While West Coast port labor talks have stalled, there was new progress in US rail labor negotiations, and workers at the Port of Liverpool canceled a planned strike this week.

Freightos Air Index air cargo rates out of China trended up last week to both N. America and to Europe, possibly indicating some peak season pick up, though rates of $5.06/kg to Europe are more than 20% lower than this time last year and China – US rates of $6.78/kg are nearly 50% lower.

Ocean Rates from Freightos.com

- Asia-US West Coast prices (FBX01 Daily) increased 11% to $2,763/FEU. This rate is 80% lower than the same time last year.

- Asia-US East Coast prices (FBX03 Daily) climbed 2% to $5,767/FEU, and are 64% lower than rates for this week last year.

- Asia-N. Europe prices (FBX11 Daily) increased 3% to $4,959/FEU, and are 65% lower than rates for this week last year.