S&P Global’s TPM24 is the major annual North American gathering of shippers, forwarders, carriers and logistic technology providers. I was fortunate to be able to attend again this year, and, though I couldn’t sit in on all the sessions or meetings I would’ve liked, here are my key takeaways:

Geopolitical challenges, Red Sea especially

Geopolitics were, of course, on people’s minds. Robert Gates, the former CIA Director, remarked that “global dangers are at a level we haven’t seen since the end of World War 2.” In addition to the Houthi threat to Red Sea traffic – which he thinks could persist even after an end to the Israel-Hamas war – he listed tensions in the South China Sea, as well as a general trend toward protectionism at the expense of the type of globalism most have gotten used to as possible threats to global trade’s status quo.

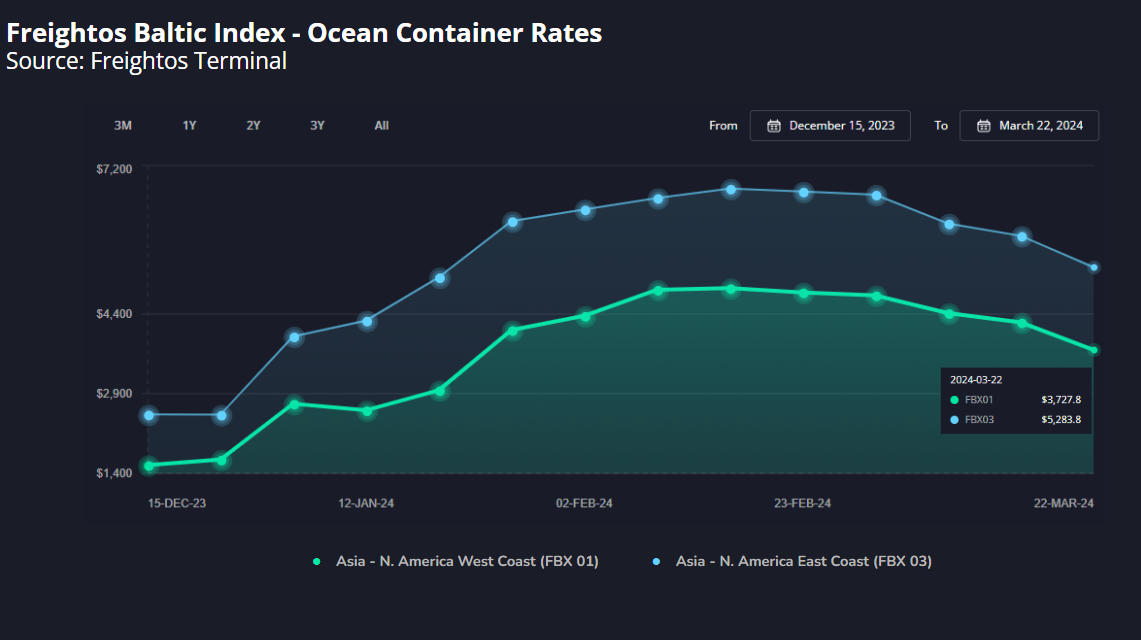

Starting with the Red Sea, ocean expert Lars Jensen, of Vespucci Maritime, argued that the disruption is really a challenge, not a crisis. It’s a challenge because it can be addressed by diverting away from the Suez Canal and utilizing more vessels sailing at faster speeds to effectively keep containers moving, even if these will mean longer lead times and higher costs while diversions persist.

But this effective adjustment is only possible due to the state of overcapacity in the market that prevailed just before the diversions and will likely return once they end. Longer routes are soaking up an estimated 16% of global capacity, according to ONE CEO Jeremy Nixon, bringing supply and demand into balance. Rates have already started to come down significantly from the initial months of the “challenge,” when uncertainty prevailed, shippers were feeling pre-Lunar New Year pressure, and carriers were still moving additional vessels into place and adjusting schedules. But Sea Intelligence’s Alan Murphy thinks rates will settle 1.5-2X their long term average while diversions continue.

Jensen also pointed out, though, that with capacity being used for diversions, there is little slack available should any additional disruption arise, and such an event really could cause a crisis.

Most experts think that readjustment once Red Sea traffic resumes will take time (up to six month according to Murphy) and will include: congestion at destination ports as still-diverted and Suez vessels arrive at the same time, empty container shortages at origins, and possible increased insurance costs. Most also agree that overcapacity will return, as will blank sailings and dry docking, though there is disagreement how significant the overcapacity will be. Consultant Jon Monroe is optimistic that carriers can reduce their charter exposure to shrink their effective fleet sizes and Jan Tiedemann of Alphaliner argued that new deliveries will be more staggered than expected, and together with an increase in scrapping could avoid an extreme state of oversupply.

Alliance shakeups, Panama Canal and East Coast labor

The conference took place close on the heels of the announcement by Maersk and Hapag-Lloyd that starting in 2025 they will partner as the Gemini Cooperation and operate a hub and spoke model of fewer origin and destinations served by transhipments from a feeder network that will deliver better utilization, schedule reliability and cost controls than the competition by using Gemini-owned terminals and feeders. Nearly all shippers who weighed in were skeptical this arrangement will succeed as most have been burned by transshipment in the past. But, aside from Hapag and Maersk, Jensen and others think it could work, given this new integrated feeder-terminal-mainline approach.

Interestingly, the drought facing the Panama Canal did not come up much and when it did was not singled out as a major concern or disruption, reflecting that the healthy majority of container traffic has continued to flow through Panama even when restrictions were at their worst – and conditions seem only to be improving as the rainy season approaches.

An issue that did come up is the looming expiration of the East Coast and Gulf ILA port worker union contract with port operators at the end of September. For the most part there was optimism that an agreement will be reached in time. But given the expiration will happen when peak season could still be going strong, the potential for disruption at that time of year may be enough to impact the market – a one day shutdown would take a week to clear. More than one expert recommended that shippers plan well ahead and that those who can should pull Q3 shipments forward to earlier in the year. There was also speculation that the West Coast could see some increase in volumes from some shift away from the East Coast.

Contracts creativity

Another hot topic that came up in several different contexts was the challenges facing shippers with long-term ocean contracts.

The fluctuations of the spot market during the pandemic, and again now with the Red Sea disruption – and really any other time spot rates have spiked or crashed – often lead to contracted volumes getting rolled by carriers or facing premium surcharges to get moved when rates spike. And when spot rates crash, carriers face no-shows from contracted shippers who’ve shifted to spot.

TPM is where many annual ocean contract negotiations get underway, and there was talk of carriers and shippers getting creative to find better solutions: Nixon of ONE said they are including penalty clauses to protect both shippers and carriers in some of their contracts, some shippers said they’ve moved away from annual tenders completely in favor of rolling one month or quarterly contracts, and others mentioned negotiating clauses specifically about Red Sea surcharges that will adjust rates down when diversions end.

All in all, both sides talked about fairness as the goal, and carriers and shippers ultimately as partners who want to help each other succeed. These discussions were particularly interesting within the context of our recent research on the state of long term ocean contracts, and the option to index-link agreements (which I heard mentioned once) and then hedge price volatility exposure through freight derivatives. You can read the report and see our short webinar on the topic here.

Progress in ocean digitalization

Discussion of the role of technology in ocean freight was more prominent at TPM than ever.

Otto Schacht, former CEO of K+N remarked that, back in 2000, he felt ocean freight forwarding was on the cusp of a major digital shift. Nearly 25 years later, he is surprised at how slow that progress has been. Nonetheless, he shared that, really, all serious forwarders can be considered “digital forwarders” today in their recognition and leveraging of digital tools to improve efficiency.

Similarly, a panel discussing the role of technology in ocean booking – including Freightos CEO, Zvi Schreiber – explored how, despite the availability of technology and gradual progress, challenges such as yield management strategies of ocean carriers and other hesitations towards true digital bookings find ocean eBookings trailing far behind air cargo. The discussion emphasized the need for a shift in attitudes among carriers to facilitate meaningful adoption.

But TPM24 also showed that – perhaps despite moving slower than many hope – digital adoption continues to march forward and tech often becomes indispensable for those who find the right solutions for their businesses. Examples included BCO and SMB forwarder presentations on the growing tech stacks they rely on to improve visibility and operations, and leading experts like Jensen and Monroe each pointing to progress in digitalization and data visibility adoption as key to carrier and BCO success.